Housing and climate are high on the political agenda in the Netherlands, and, as the “financial engine” of the public sector, BNG Bank’s ESG bond issuance is both reflecting and supporting these and other societal goals. BNG’s Rob Schreppers, Sydney Siahaija and Koen Westdijk spoke to Sustainabonds’ Neil Day about its impactful and innovative lending, global trends driving market dynamics, and the strategy behind its growing social and sustainable issuance.

A pdf of this article can be downloaded here.

Neil Day, Sustainabonds: How important is ESG to BNG’s mission? And how is your activity developing in the current political climate?

Rob Schreppers, head of relationship banking, BNG: BNG Bank is the financial engine of the public sector, encompassing municipalities, social housing associations, healthcare, water companies and the like. And in the Netherlands, ESG is for all those organisations very important — at least implicitly, and increasingly explicitly.

Take our biggest client base, the housing associations, for example. We are their most important lender, with a 60% share and some €7bn-€8bn a year. Their main operation is renting out houses — 2.4 million of them, maintaining these, and ensuring that there is additional housing. They have agreed with the government that every house — existing as well as new — reach an energy efficiency level of at least A, B or C before 2030. Therefore, any investment they make is always based on energy efficiency. So, as you can see, ESG is not only implicitly important, but very explicitly so. And it is a key part of their mission: housing costs are not only a question of rent, but also the monthly costs associated with living in the property, and energy bills are a very important part of that.

It’s the same if we look at healthcare. Healthcare is challenging, because there’s a lot of demand — more than we can afford — but for every process they operate, whether it’s in the operating theatre or new buildings they develop, energy efficiency, water, pollution, everything like that is prominent in everyone’s thinking.

Beyond that, ESG has multiple aspects. What I have spoken about is the “E”: making sure housing and healthcare is very well maintained, energy efficient, and everything related to that. Then “S”, it’s what all our clients’ efforts are directed towards. We think that 2.4 million houses are needed to ensure everybody has a decent home. They need to make sure that they’re doing an efficient and economical job, of course, but the S is never up for discussion. Finally, the “G” is hardly discussed in the Netherlands, because we are always very well organised and like to keep track of everything.

When the “E” side was emerging as an important topic a few years ago, I expected that it would lead to difficult discussions for my relationship managers with our clients, because there are limited funds available for them to do their jobs, and now somebody is coming along with additional demands that might prove expensive. But I was quite happy to find that the opposite is true: all our clients believe this to be one of their priorities. Whether for housing, healthcare or municipalities, their tasks may be a little more difficult, but they understand that it is really important. So we want the same thing. The only discussion is at what pace. All of our clients are aligned with the Paris Agreement — maybe not every year, but on average, it’s the pace they set. So I’m quite optimistic, because even if it’s a tough job, everybody is taking their responsibility seriously.

Koen Westdijk, head of treasury, BNG (pictured): The importance of ESG to our mission and strategy remains undiminished. Questions are sometimes raised about whether ESG continues to be the right direction, but within the EU and the Netherlands there is a clear and sustained commitment to ESG principles, including in the financial markets. This is also reflected in the expectations and priorities of our clients, as highlighted earlier.

Investor demand confirms this picture. Interest in our ESG-labelled issuance remains strong, although there are regional differences. Asia and Europe continue to show consistent and robust support for ESG, while demand from other regions varies. Overall, ESG remains a relevant and valued element of the investment universe.

That said, it is important to acknowledge the broader global context. Achieving collective goals, such as those set out in the Paris Agreement, requires coordinated international effort. If progress differs significantly across regions, this may affect both the pace and the overall effectiveness of the transition. Sustained collaboration across economies will therefore be essential to meet shared long-term objectives.

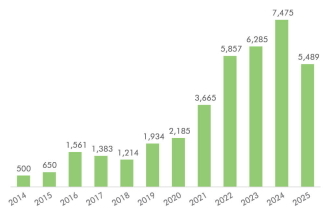

Sydney Siahaija, head of funding, BNG: We launched our first ESG bond in 2014, the year we published our first sustainable finance framework. We started with €500m, but since then we have been issuing ESG bonds every year, and the amounts have been going up almost every year. In the past couple of years, ESG bonds have represented about 30%-40% of our long term issuance, so we’re talking €5bn-€7bn a year — quite a substantial amount.

BNG ESG issuance (EUR m equivalent)

Source: BNG Bank

By and large, as Koen said, we definitely still see very strong support for these bonds. That’s partly due to some investors having specific mandates to buy ESG bonds. Indeed, BNG has a very diversified investor base across both geographies and different types of investors, and we see that there is a pretty wide spectrum of interest in ESG products among these varied investors. Some asset managers, for example, may have specific kinds of ESG mandates, while others, such as bank treasuries, may have specific ESG targets as a percentage of their liquidity portfolios. There’s always going to be investors on all parts of the spectrum, so not every investor is going to be interested in ESG to the same extent as these ESG-only mandates.

We also see diversification across the globe, so that even if some regions may be on the whole more invested in ESG products — as Koen rightly mentioned — we do see very ESG-focussed investors in all geographies. And it’s always great to have the opportunity to share with investors across the globe the story that Rob described earlier, because ESG is very much a part of BNG’s DNA.

Day, Sustainabonds: A new coalition government was recently formed in the Netherlands. What are the implications for you? And more generally, in Dutch politics you tend to have a new government being formed every four years — how does this affect you?

Westdijk, BNG: The current coalition places a stronger emphasis on climate action than the previous cabinet, reflecting a continued upward trend in national climate ambition over the past decade.

When it comes to housing, this has been a big theme for the previous coalition as well as the current one. We have a major housing shortage in the Netherlands: the Dutch housing stock consists of 8.3 million homes in total, of which 2.3 million are social housing units — roughly 28% of all homes. In spite of this substantial social housing sector, the country still faces a shortage of over 400,000 homes.

So a big theme in the elections was housing, and affordable housing, and this is very relevant for our biggest client group. Housing associations will play an important role in helping to solve this problem and we therefore anticipate an increase in their activity — and certainly not a decrease — and hence in our lending to this major client group.

Schreppers, BNG: One of the main advantages of the Dutch system with multi-party coalitions is that the direction always remains more or less the same. We stay in the middle of the road, with some room for small diversions. For example, energy is today a bit more of an issue than it was perhaps two years ago.

I expect our housing portfolio to grow significantly for at least the next three to five years, a few billion a year, because it’s essential — it’s as simple as that. Housing is one of the main topics in Dutch politics. If you go to a birthday party with your kids, it’s what all the parents are talking about. I have older sons, so I see the problem — it’s almost unaffordable. Likewise for energy: there are parts of the Netherlands where it’s impossible for companies to get connected to utilities. These are critical issues for our children, for our livelihoods, for our economy.

And they are topics that are uppermost in the minds of our clients in the public sector, in the housing associations, healthcare, municipalities. The discussions that I have are, how do we make more investment possible? And, are there smart solutions available for the Dutch government or municipalities to make greater impact with their investments? So it’s about doing more, not less.

Day, Sustainabonds: Can you share any recent examples on the lending side of concrete actions you are taking to help your clients achieve these ambitions?

Schreppers, BNG (pictured): Indeed, we want to support our clients in achieving their goals and moving more rapidly towards the Paris Agreement targets, so the question for us is, how can we, as BNG Bank, do so?

Koen and Sydney have described our offering on the funding side and how it has developed, and they are doing their best to enable us to offer cheap financing to the public sector, thereby enabling bigger investments in housing, healthcare, and so on.

Koen and Sydney have described our offering on the funding side and how it has developed, and they are doing their best to enable us to offer cheap financing to the public sector, thereby enabling bigger investments in housing, healthcare, and so on.

We are meanwhile playing our part on the client side. For example, today we launched a new green loan, a special product for housing associations. If they reach certain parameters, they are eligible for a discount on the loan.

When we were designing the product, we wanted to make sure that it would not be burdensome for our clients, in terms of administration or expense. So we spent a lot of time with the housing associations and other stakeholders discussing what information they already have, how we can use it, and what the parameters should be. They have a wealth of data from the 2.4 million housing units, but the question was, what are the key numbers that will help us really stimulate construction of the right buildings, those that are more climate neutral and energy efficient? And we succeeded in finding appropriate parameters that all the housing associations already had, without requiring further work or expense on their part.

And then we had to tackle the fact that there are two kinds of financing for housing associations: the loans guaranteed by the WSW (Social Housing Guarantee Fund), and then the classic security-based bank financing. We wanted to create something that would be useful for each of them, to both address the needs of seniors, for example, and ensure that a policeman can afford a house in the city.

Ultimately, we had four pilot schemes taking in the various sectors and found that we had successfully achieved our targets. The product worked for everyone and made possible investments that without the discount would not have been feasible. We therefore decided to launch the green loan.

It is important to note that, contrary to some expectations, there is no additional cost for the loan at the start. Borrowers will get a normal, competitive market rate, and then if they hit the target, they get a discount. That is important because it’s our obligation as BNG Bank to ensure that borrowers are financed at the lowest possible rate.

We started with the housing associations for this green loan product because it is the largest sector we finance, but I expect that at the end of the year we will have a similar product available for more client groups.

Day, Sustainabonds: Sydney, you mentioned how long you have been active in ESG bonds. How has your issuance changed over the years?

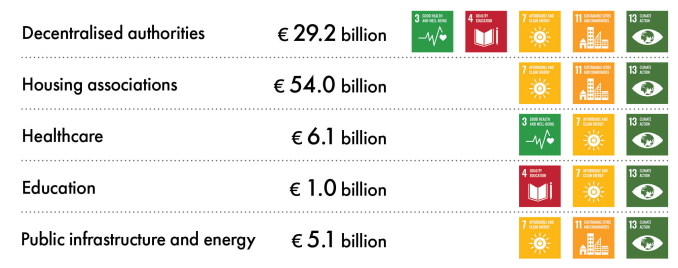

Siahaija, BNG: The original framework that we published in 2014 was a best-in-class framework. We looked at the entire population of municipalities and housing associations in the Netherlands, compared them based on various metrics, and selected the top percentile to finance with our ESG bonds. For the municipalities, we issued sustainability bonds, and still do, while for the social housing associations, we issue social bonds.

But in 2021, seven years after creating the initial framework, we published a new one. This was no longer a best-in-class framework, but rather sought to finance all the municipalities and social housing associations — which makes a lot of sense given that all our clients contribute to sustainable and social goals. To this end, we looked at the expenditures of these client groups.

For the housing associations, we only finance with our social bonds loans that are guaranteed by the WSW. This fund has specific criteria for the types of loans that it can guarantee, they have to be for a social purpose, for example, building social housing in the Netherlands, maintaining this housing, or increasing its energy efficiency — which is actually a dual purpose. We were thereby able to link the expenditures of the social housing associations to the Sustainable Development Goals of the United Nations.

We did the same type of exercise for the municipalities, linking their expenditures to the SDGs. We found that about two-thirds of their expenditures could be directly linked to the SDGs (this number is updated every year based on the budgets of the municipalities) and those are the expenditures that we finance with our sustainability bonds.

BNG loan portfolio and main SDGs per core sector

Source: BNG Bank

That’s the framework we’ve been using since 2021, still issuing under the two labels we have been using since the beginning of our ESG adventure. We published an update to our framework in 2024, but this was more of a version update to bring it more into line with the latest developments — the ICMA standards, for example, are also ever-developing — and we also got a new second party opinion to go with that.

Day, Sustainabonds: We have seen issuance of EU Green Bonds (EuGBs) picking up. How do you view their introduction and related initiatives such as the EU Taxonomy? Is it something for BNG?

Siahaija, BNG: That’s a very good question. What’s important to understand is that BNG, as a public sector agency and public sector bank, finances our clients on a budget basis, not on a project basis, as is the case for some other issuers, such as those that have been active in the EuGB space. SNCF, for example, can identify exactly the money that went towards the purchase of some specific trains, and hence has a very clear-cut case of something that is Taxonomy-aligned and can be used for an EuGB. But for BNG and the many other European public sector banks out there with a similar way of operating, it is quite challenging to be able to issue an EuGB because of these strict taxonomy alignment requirements which are more geared towards projects. That is definitely something that we would like to be addressed in the future, and we are working with the Dutch Banking Association and European counterparts to help develop the space such that the social and sustainable uses of proceeds of European public sector banks can also qualify, because that would be useful in developing the space for everybody. Achieving more harmonisation through the EU Taxonomy and Green Bond Standard has definitely been a great step forward and the sector was definitely looking for that, but it’s only to be expected that this is a developing space and that we’re going to see further steps in the future.

Day, Sustainabonds: What market dynamics have you noted in the execution of your more recent social and sustainable bond issuance?

Siahaija, BNG (pictured): Certain currencies still demonstrate a preference for an ESG label — Canadian dollars and Australian dollars, for example. In these currencies, it’s not a prerequisite, but many of the most relevant investors that you would like to see in the book have a very strong preference for ESG-labelled paper. But BNG has been active in issuing ESG bonds across almost all currencies and also tenors. For example, the largest deal we issued in ESG format last year was actually in US dollars, a $2.5bn (€2.16bn) five year social bond.

Siahaija, BNG (pictured): Certain currencies still demonstrate a preference for an ESG label — Canadian dollars and Australian dollars, for example. In these currencies, it’s not a prerequisite, but many of the most relevant investors that you would like to see in the book have a very strong preference for ESG-labelled paper. But BNG has been active in issuing ESG bonds across almost all currencies and also tenors. For example, the largest deal we issued in ESG format last year was actually in US dollars, a $2.5bn (€2.16bn) five year social bond.

As I mentioned earlier, we see global participation in our issuance from many different types of investors, with a greater or lesser focus on ESG. Investors for whom ESG is maybe not such a requirement nevertheless acknowledge that our ESG lines have liquidity that is as good as, if not greater than that of our regular lines — which make sense, if you consider that the number of investors who are able to buy them is greater. That’s definitely something we typically see in bookbuilding for an ESG line, more different investors, and some investors also being able to upsize to a larger order. That’s also ultimately reflected in secondary markets, where investors are simply going to have a slight preference overall for those ESG bonds.

Day, Sustainabonds: Does your issuance enjoy some kind of greenium? Also, we have seen some issuers choosing to issue labelled bonds at times when markets are more volatile, considering them less risky — does this chime with your experience?

Siahaija, BNG: It’s quite hard to say if there is a real greenium in a specific market at a specific time. You would really have to issue both types of instruments at the same time, like the German state has done, in order to say for sure. But, as I mentioned, while we see very strong demand for our regular bonds, demand for our ESG bonds is a little stronger, and in some cases that could ultimately lead to such a bond outperforming slightly.

We haven’t issued a labelled bond into a market where we would not be comfortable issuing a regular bond, so in that sense, I don’t see it as a very important de-risking tool. But I would say that if you do decide to use a label, it does typically feel like a bit more of a “sure bet” kind of transaction, because — for the aforementioned reasons — we typically see the slightly larger order sizes and/or a greater number of lines, and hence enjoy a stronger bookbuilding dynamic.

Day, Sustainabonds: What is your funding programme for 2026, and what part does ESG issuance play within this?

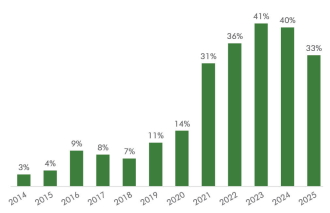

Siahaija, BNG: The programme this year is expected to be between €15bn and €17bn. That’s very much in line with what BNG typically does, in the €15bn-€20bn range. So far this year (as of 17 March), we’ve done about €3bn, which we think is a healthy pace, and we’ve had continuous access to funding throughout the first couple of months of this year.

BNG ESG issuance as a percentage of total issuance

Source: BNG Bank

In terms of the ESG issuance, we would expect it to also be in line with previous years, around 30%-40% of our funding. That’s been a relatively steady state for us. It’s also a result of the fact that we only have the programme in place to finance two of our client groups, so not all of our client groups, and also because we only finance the expenditures of the municipalities that we can link to the SDGs, rather than all of their expenditures.

And then we also don’t refinance existing loans with ESG bonds once an initially-issued ESG bond matures. For example, if the initial ESG bond that we allocate a loan to is, let’s say, five years, whereas the loan is 10 years, after five years the bond matures and the loan still has five years to go, but we don’t allocate the remainder of the loan to a new bond, because we want to only allocate new loans to our ESG bonds.

Day, Sustainabonds: As well as ESG-related sustainability, debt sustainability has become an issue for the SSA sector in recent years, with supply contributing to upward pressure on spreads. Has this affected you?

Siahaija, BNG: Issuance levels for us this year have largely been trending down in spite of the ongoing geopolitical situation, the war in Iran.

Debt sustainability in the government space has indeed been a very relevant topic in the last couple of years, and will continue to be relevant. Headlines right now are very much focused on other things — which makes a lot of sense — but once you get to 2027, you might see more focus again on the French election cycle and French debt sustainability, for example, which is a very important topic for debt sustainability for the European Union as a whole. So I don’t think these topics are going to go away in the near term.

As Rob explained earlier, BNG operates in the Netherlands, with its coalition government system, which ultimately leads to a high degree of stability. This stability is not only applicable to the topic of ESG, but also with regards to fiscal discipline. Being frugal is very much ingrained in Dutch culture. And that has led to fiscal deficits below, or even well below the 3% level in the Maastricht Treaty that is applicable to all European member states, but which only a few adhere to, the Netherlands among them. That is why we currently still have debt-to-GDP of 45%, which is among the lowest in the union, and also among the lowest globally.

Given that backdrop of fiscal responsibility, BNG and the Netherlands are very well positioned to weather this increasing debt sustainability issue — that’s very important in reassuring our investors now, but also in the future.

Dutch social housing featuring energy efficient improvements supported by BNG; Source: BNG Bank

Sustainabonds conducts all research and writing independently to maintain the full editorial integrity of the publication.

As a supporter of Sustainabonds, LBBW is facilitating a series of interviews with leading players in ESG and the green, social and sustainability bond markets.